DPA

An April 1 demonstration in Lisbon against high unemployment and the government's austerity measures. Last week, Portugal became the third euro-zone member to ask for a bailout.

Wolfgang Schäuble hates being disturbed on Saturday afternoons. That's when Germany's finance minister, a huge soccer fan, likes to watch the games of his favorite team, Bayern Munich, on TV.

On Saturday April 2, Schäuble's job obligations spoiled his fun when he was forced to take part in a conference call. Waiting on the line were his colleagues in other important euro-zone countries, including French Finance Minister Christine Lagarde, European Monetary Affairs Commissioner Olli Rehn and Jean-Claude Trichet, president of the European Central Bank (ECB).

The reason for the disturbance was a crisis that had already ruined many of Schäuble's weekends in recent months — even more so than Bayern's crummy playing this season: Once again, it was about the state of the European monetary union and the issue of how financially troubled member states should be assisted.

After a year full of financial woes, cash shortages and near-bankruptcies, the situation has become anything but reassuring. In fact, in recent weeks, the euro crisis has gotten even worse.

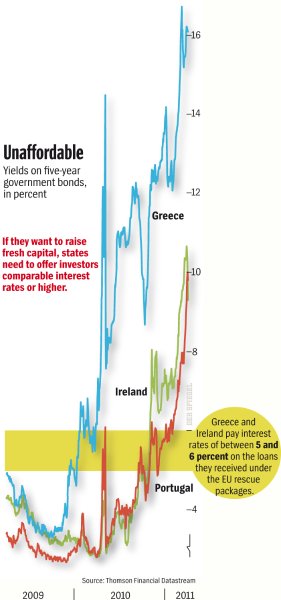

Graphic: Yields on selected euro-zone debt

Graphic: Scope of the EU rescue packages

Following months of insisting it would not need a bailout, debt-stricken Portugal has now asked for help from the European Union's euro rescue fund. In a television address last Wednesday, Portuguese Prime Minister Jose Socrates announced that his caretaker government could no longer deal with the pressure from the financial markets by itself. Before making the announcement, yields on the country's sovereign bonds had climbed to almost 10 percent, a new record.

Indeed, on the whole, those in charge of rescuing the euro in Brussels and Europe's capitals have done a poor job. So far, almost all of their expectations have been disappointed. And things have continuously gotten only worse.

At first, people thought that the European Financial Stability Facility (EFSF) — the temporary rescue fund that will be replaced by the permanent European Stability Mechanism (ESM) in 2013 — had been equipped with enough resources to calm the markets, and that no one would actually draw on its help in any case. But, now, two countries, in the form of Ireland and Portugal, have asked for support, and no one can say for sure that they will be the last.

Admission of Failure

Even worse, however, is the situation in Greece. Last year, the European Commission, the ECB and the International Monetary Fund (IMF) assembled a special rescue package for Greece in order to help it avoid defaulting on its loans. But, since then, things haven't gotten much better.

After a year of financial adjustments and reforms, prices for Greek sovereign bonds are lower than they were when the rescue effort was launched, and their yields have reached record highs. Indeed, the country's government has almost the same credit ratings as it did 12 months ago.

This development can be seen as a vote of no confidence by investors in the EU's rescue measures. Players on the financial markets simply don't believe that Greece will be able to stand on its own two feet any time soon. And now there is the risk that something will happen that the Europeans already tried to prevent last year, namely that Greece will be forced to restructure its debt.

Despite all the denials, there is a growing realization that a so-called haircut can no longer be avoided. SPIEGEL reported last week that the IMF is putting pressure on Athens to restructure its debt. And it's not just the IMF that is pushing for Greece to take a haircut: Among euro-zone finance ministers, too, support is growing for the radical solution, which would involve holders of Greek sovereign bonds taking losses.

Last week, during a meeting of the European Commission, European Monetary Affairs Commissioner Olli Rehn told his colleagues that they shouldn't speak publicly about a Greek debt restructuring, but that a restructuring would have to be carried out in good time. If things really came to that, he said, it would be nothing less than an admission that the euro zone's approach to fighting the crisis had failed, at least in the short term.

Growing Deficit

The issue of restructuring Greek debt also came up in Schäuble's conference call. He and some of his colleagues expressed their unease about developments in Greece and voiced skepticism about whether the reform measures would ultimately succeed.

Their doubts are justified. Indeed, the most recent analysis by the European Commission, the IMF and the ECB on the issue of whether Greece will be able to refinance its debts by itself came to an alarming conclusion. The study found that the country's economy is contracting more than previously feared and that one of the main causes behind the contraction was the harsh austerity measures that the government has been forced to introduce in return for receiving outside assistance. As a result, the public deficit in Greece has climbed even higher than previously assumed.

The expert report also says that Greece's program for sorting out its finances has reached a critical phase. In order for the country to be able to handle its debt burden by itself, its economy will have to pick up and there must be an increase in the country's notoriously uncertain government revenues. But, at the moment, neither of these things is happening. During the conference call, some finance ministers very gingerly suggested that, given the situation, it might make more sense to let Greece restructure its debt.

"I'm not prepared to talk about that," ECB President Jean-Claude Trichet barked into the phone. If creditors grant Greece's request for a reduction in the amount it owes, he argued, the entire euro zone could face a crisis of confidence.

Impact on ECB's Profits

Trichet also warned that such a step could hit banks that hold a lot of Greek debt hard. Nevertheless, these worries did not prevent Trichet from announcing on Thursday an increase in the interest rate in the euro zone, thereby worsening the financial crises in the debt-stricken countries.

This is one reason why Schäuble thinks that Trichet's worries about the markets are exaggerated and lack credibility. What's more, he knows that Trichet's actions are driven by another motive, albeit one that he never openly admits: As part of its measures to bolster Greece, the ECB bought up several billion euros worth of its sovereign debt. For that reason, it is one of Greece's creditors itself and would therefore also be affected by a Greek debt restructuring. The ensuing write-downs would noticeably reduce the ECB's profits — something Trichet would like to avoid at all costs during his final year in office as the bank's president.

In fact, Schäuble and his colleagues are getting increasingly angry with Trichet. As they see it, if Trichet is going to be so dogmatic about rejecting a Greek debt restructuring, then he has to explain how Athens is supposed to be able to raise money on the markets by itself as early as the start of 2012, as envisioned in the plan for sorting out its finances. The finance ministers argued in the conference call that that is nothing but wishful thinking.

The only other possible alternative to a controlled default for Greece is additional financial aid for the country. But Schäuble has already made it clear to Trichet that he is highly unwilling to grant the Greeks another round of help. Schäuble justifies his refusal with the argument that he would never get additional aid for Greece through the Bundestag, the lower house of Germany's parliament.

Resistance to providing Greece with any more help is particularly pronounced among members of the business-friendly Free Democratic Party (FDP), which governs in Berlin as the junior partner in a coalition with Chancellor Angela Merkel's center-right Christian Democratic Union (CDU) and its Bavarian sister party, the Christian Social Union (CSU). "In the interest of the German taxpayer, Greece cannot be allowed to receive even more money from its European partner countries," says Volker Wissing, an FDP politician who is head of the Bundestag's finance committee.

"If you subscribe to the faulty logic that you always have to help, then you will always have to keep making more payments," says FDP financial expert Frank Schäffler. "In doing so, the community of states opens itself up to blackmail — not only from banks, but also from the countries it helps."

The opposition is also concerned. "In the light of the underlying economic data, Greece will not be able to survive in the medium term without restructuring its debt," says Carsten Schneider, budget spokesman for the parliamentary group of the center-left Social Democratic Party (SPD). He adds that it is no longer justifiable to use "taxpayer money to relieve banks and other private creditors by extending public loans to Greece."

Since other donor countries are hardly more willing to come to Greece's aid, Schäuble and his foreign colleagues more or less agree on where things should go from here: Although Greece's government cannot be forced to restructure its debt, no one can stop it from entering into voluntary talks on the issue with its creditors.

Barroso Sent to Lisbon to Whip Up Support

Even if the finance ministers can't force Greece to do anything, in the case of Portugal they considered a bit of pressure to be long overdue. They unanimously turned down the Portuguese request to receive a bridge loan without any conditions so that the country could survive the period until new elections in June.

Instead, the finance ministers decided that it would be much better for the Portuguese to follow the designated path of requesting assistance from the European Commission and the European rescue fund. But to receive any of this help, Portugal had to agree to certain conditions that the caretaker government of Prime Minister Socrates would have preferred to avoid. To bring the recalcitrant Portuguese in line, the finance ministers decided to send Jose Manuel Barroso, the president of the European Commission, to his home country to try to whip up support for their plan. Though he wasn't thrilled about it, Barroso went to Lisbon and spoke with representatives of both the government and the opposition.

Last Tuesday, the heads of Portugal's five largest banks informed Portuguese Finance Minister Fernando Teixeira dos Santos that they couldn't lend the government any more money. Bank executives told the government that things had gotten too risky, pointing out that they already had €14 billion ($20 billion) in sovereign debt on their books. On Wednesday, Barroso reported that the proud Portuguese had finally buckled and that the plan could go forward.

Conditions Unclear

Two days later, Portugal's formal request for aid arrived in Brussels. The finance ministers of EU countries, who were holding a meeting near Budapest at the time, instructed European Commission experts to evaluate the request for aid as quickly as possible.

On Friday, the finance ministers meeting in Hungary announced that Portugal would need €80 billion ($115 billion) in aid. But it is unclear which conditions will be attached to the aid package. The Portuguese have yet to allow any IMF officials into the country. The plan is to send a group of investigators — or "mission" —from the IMF, the European Commission and the ECB to Lisbon in the next few days to figure out exactly what the country's financial situation is. A plan for rehabilitating the country's finances should be developed by mid-May. Only when that is ready can money start flowing to Lisbon.

While the finance ministers are happy about the decision, others worry that the elections planned for early June could lead to attempts to renegotiate the rescue package. The same thing recently happened in Ireland, where the new conservative government in Dublin is still hoping to amend some of the conditions imposed on Ireland in return for aid.

Fears Turned Out to Be Justified

However, something that worries the Europeans even more is the possibility that Portugal won't be the last country to ask for a bailout. Belgium and Spain could also find themselves in dire financial straits.

On the positive side, Spanish Finance Minister Elena Salgado stressed that the risk premiums the Spanish government has to pay on its sovereign bonds have dropped 30 percent since the start of the year. And even on Wednesday, the day that Portugal threw in the towel, interest rates on Spanish bonds fell.

But, even so, many still think that Spain is at risk of falling into financial distress. Their pessimism is born out of bitter experience: So far, all of the fears during the euro crisis have turned out to be justified.

If Belgium and Spain really do run into financial trouble, it would present the other euro-zone countries with a whole new series of challenges. By then at that latest, EU finance ministers will have to deal with the issue of beefing up the rescue fund. Until now, they have been procrastinating on addressing the problem.

Taking the Euro Fund to Court

As of Monday, it won't be just EU finance ministers busying themselves with the issue of financial assistance for Portugal. It will also be Germany's highest court, the Karlsruhe-based Federal Constitutional Court. Markus Kerber, a constitutional lawyer and financial expert from Berlin, wants the court to issue a temporary injunction forbidding the government from agreeing to financially assist Portugal.

In a 37-page legal brief, Kerber say that if the court cannot bring itself to block the move, the danger will arise "that, after the Republic of Ireland has taken advantage of the 'European Stability Mechanism' and the Portuguese Republic has filed a request (for such aid), we can count on similar requests coming quickly from the Spanish, Belgian and even Italian governments."

Last year, Kerber and roughly 50 supporters filed a constitutional complaint against the euro rescue fund. He fears that the ongoing proceedings in Karlsruhe will become pointless if one country after the other seeks help from the rescue fund. "What is the Federal Constitutional Court supposed to rule on," Kerber asks, "if the majority of the money has already been paid out?"

Translated from the German by Josh Ward.

Part 1: Greek Debt Restructuring Looks Inevitable

Part 2: Germany Unwilling to Provide More Aid for Greece

Part 2: Germany Unwilling to Provide More Aid for Greece

©spiegel.de

Price: $1,399.99

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.